Following a significant number of enquiries within the superannuation industry, the Government sought industry comments on an Inquiry into the Adequacy and Efficacy of Australia’s Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) Regime. This poses the question “what will the future of AML/CTF in Australia look like?“

The legislation, requiring reporting entities (including regulated superannuation funds), to mitigate and manage the risk of money laundering and terrorism financing has been in place since 2006. There have been several reforms since, and most have been underpinned by:

reviews undertaken by the Financial Action Task Force (FATF) to assess Australia’s compliance with their recommendations; and

recommendations from the Report on the Statutory Review of the AML/CTF Act 2006.

Fortunately, we have not had a major terrorism event in Australia, however we have seen significant breaches of the law by two of our big four banks. Westpac admitted to breaching the law more than 23 million times in 2020, resulting in a record $1.3 billion penalty. This followed CBA’s $700 million penalty in 2017 for failing to report millions of dollars of suspected money laundering activity.

This year, FATF produced several publications to highlight emerging challenges in the AML/CTF space, including the Opportunities and Challenges of New Technologies for AML/CTF.

Technology is a common theme emerging from FATF analysis, and it is proving likely that this will be the key to mitigating money laundering and terrorism financing risk in the future.

In FATF’s view, the main challenges hindering the effective implementation of AML/CTF measures are:

a poor understanding of the threats and risks around money laundering and terrorism financing (ML/TF);

a lack of flexibility in risk assessments (based on static analyses of pre-determined data combined with human judgement);

decision making based on inadequate risk assessments and a heavy reliance on human input; and

the inability for data to be analysed at a large scale.

New technologies used in the identification, assessment and management of ML/TF risks, allows risk analysis to be:

more dynamic;

provide network analysis; and

operate at customer, institutional, jurisdictional and cross-border levels.

That said, optimal use of these tools requires a regulatory and policy environment that frames adequate pooling and sharing, or collaborative analytics, as well as appropriate access by law enforcement.

FATF analysis has found that the two most important preconditions, to enable adoption and use of new technologies in the AML/CTF space, are favourable regulatory frameworks or incentives and competitive costs.

So what can we expect from the inquiry?

It’s reasonable to anticipate that we will have to change. The indications from the FATF findings are that to manage ML/TF, organisations need:

a robust programme that is not static,

to be capable of extensive analysis,

less reliance on human intervention, and

regulatory changes that support this approach.

The enquiry findings are due to be published on 2 December 2021.

Recently ASFA’s CEO Martin Fahey called out that the trustee office of the ‘not too distant’ future will need to be much more sophisticated. He was referring to the increasingly strategic role that a target operating model plays in the reformation of funds faced with new operating challenges, underpinned with new or refreshed technology options.

At IQ, we are seeing this challenge every day – where our customers look to reflect their value chain in their approach to their admin ecosystem, investments and insurance. We echo Martin’s view, especially in the area of administration, where being a ’service integrator’ is becoming one of the key factors in member services delivery and efficiency.

Too often we see this discussion polarised and simplified. ‘Outsource’, ‘Insource’ or ‘Hybrid’ may be an easy way to paint what is a complex picture. It misses a key issue. Before a super fund decides on these things, it should consider the enterprise capabilities required, and more importantly, which ones it needs to own to be more than justa parity player in the new landscape.

Options for approach, a strong understanding of the future obligations and responsibilities, and continuing waves of regulation are forcing funds to carefully reconsider their strategy and try to clearly understand how their choice of capabilities/operating model impacts on member outcomes now and in the future.

There is no standard approach and each client creates an individual pathway to success.

For the last three years, IQ has worked together with funds to undertake some of the biggest changes in their history. What is common to achieving success, is fundamentally a strong understanding of strategy and how it impacts on a fund’s products and services and the capabilities that need to be changed or developed.

There are three key areas that support decision making, when it comes to any administration transition:

Understanding legacy decisions

This is the less glamorous side of transitions, but is the area that derails them most. Understanding legacy operations and technology, means a conscious process of prioritising the new world, rather than just paving the cow path with new tools. In its 20 plus years, IQ has been a part of (what is now) legacy implementations and migrations. Understanding why certain decisions were made in the past is critical to making the right decisions for the future

2. Understanding how technology empowers service

The decisions about technology must be made to serve the fund and its members. To not challenge the assumptions about technology (which are mostly dated, here say/anecdotal or at worst prejudice), means that decisions are not data driven and are less likely to be future ready. It’s a costly mistake to make. Technology needs to be proven at both diversity and scale before being considered. However, it’s the successful integration of service and technology platforms that provides the value necessary for funds to remain competitive in the long term.

Our recent experience shows that achieving breakthrough service and efficiency in transitions, is not based on how “digital ready” a fund is, but how ready to embrace RPA and machine learning it is, outside the technology.

3. Understanding roles and responsibilities

The regulatory burden for funds continues to increase, as pressure is firmly placed on performance and associated data transformation and reporting requirements. Add to this complexity of transition approaches and funds are confronted with a varying array of roles and responsibilities.

In choosing which capabilities or operating model is best, a fund needs to be clear on the roles and responsibilities it will be taking on, under each approach. Each variation comes with a differing set of responsibilities. This applies beyond regulatory responsibilities to those around technology and service and how the two are integrated, both at the outset and in the years that follow.

The options for super funds are very broad. No longer are funds buying off the showroom floor as each option comes flat packed. It’s only with the support of trusted partners that a cohesive model can be built successfully (and without pieces left over).

Innovation occurs when the strategy is clear, capabilities are aligned and there is an operating model that flexes and bends in whatever direction is needed for future growth.

After 20 years in business, IQ is at the forefront of change through a deep understanding of superannuation legislation as well as current and emerging trends (be it economic, technological or social). We take a proactive approach to addressing the impacts of change in the superannuation industry and on funds of all categories and sizes.

Whether it’s a merger, acquisition, re-platform, technology refresh, change in service partner or a remediation exercise, IQ is the only consultant with strong domain expertise in superannuation; with an understanding of how current and emerging technologies integrate into service; and with an intricate knowledge of regulatory and legislative requirements.

Combine our tried and tested methodologies with our clarity, and the result is confidence and success.

It wouldn’t be budget night if there weren’t a raft of superannuation announcements, and tonight’s Budget didn’t disappoint. This blog isn’t so much about what was announced as it is about the work that super funds need to do to put the announcements in place.

However, while most of the announcements require new laws to be passed by Federal Parliament and will get lots of media coverage, most require relatively small effort to implement on the part of super funds and administrators.

SG contributions to be increased from 9.5% to 10% from 1 July 2021

The Budget papers don’t mention the legislated increase in the Superannuation Guarantee – meaning that it’s increasing to 10% on 1 July. Legislation, to give effect to the increase, is already in place, and no action means … it’s going ahead.

Employer payroll software already anticipates this (and subsequent) increases and so the increase will occur seamlessly. The level of SG contributions received by super funds will increase but this will not require any system or process changes.

The Government hasn’t announced any moves to stop future SG increases in the Budget, although they may do so in the future. Some on the Coalition backbench are on the record that they want to see the SG frozen at current levels, but they haven’t prevailed tonight.

Current law provides that the SG will increase by 0.5% in each subsequent 1 July until it reaches 12% on 1 July 2025.

Removal of the $450 per month income threshold to receive SG contributions

Many workers in very low paid jobs, or who work in multiple jobs at the same time, will be receiving superannuation contributions, many for the first time.

Hundreds of thousands of new accounts are likely to be created. These new accounts are likely to be subject to the 3% fee cap introduced by the Protecting Your Super laws for accounts with account balances less than $6,000. The large number of new accounts, and the fee cap, may require super funds to review arrangements with their outsourced administrators.

As many of these new members may have short term employment and may be more itinerant than the overall population, it may be more difficult to get and maintain their details. This will also have cost implications and put pressure on administration arrangements. Fund communications about superannuation rules and employer obligations will have to be reviewed and changed.

Overall, however, super funds will welcome this measure as it means that even low-income workers will receive an additional supplement on retirement, and the compulsory superannuation system takes another step towards greater universality.

Increasing the voluntary super that can accessed under the First Home Super Saver Scheme from $30,000 to $50,000

This measure is a small change to the early release of superannuation arrangements. It does not open up access to superannuation for housing on a widespread basis. It is much less of a change than some commentators had predicted.

Although the First Home Super Saver Scheme has been in place since 2017, it has had a very low take-up rate. The Budget announcement increases the amount of superannuation that can be accessed, but this needs to be changed in the applicable law. Our crystal ball is telling us that the level of take up is going to continue to be small and won’t have any impact on housing affordability.

Most of the administration for the scheme will continue to be done by the ATO, and funds will not be stressed implementing this change. SG contributions cannot be accessed under the scheme, only voluntary and salary sacrifice contributions. This change will have very little administrative impact.

Work test abolished for people aged between 67 and 74 years

Super fund rules and processes need to be reviewed to accommodate this change, along with fund letters and communications. Super funds won’t need to ask these older members if they meet the work test. This will simplify the administration arrangements in engaging with older members.

Lowering the access age for the home downsizing age from 65 to 60 years

The home downsizing measure is already in place for people aged 65 years and older. The rules around the treatment of proceeds paid into super are well established (eg. payments are not treated towards either concessional or non-concessional contribution caps). People using this will have to provide the same documentation to support eligibility for it, as for the existing measure.

2 year transition of legacy retirement product members to better products

People in market-linked, life-expectancy and lifetime products (commenced prior to 20 September 2007) will be able to leave these products for more flexible retirement products on a voluntary basis. Legislation is needed to give effect to these changes.

The process of transition is likely to be complicated and potentially tricky. Funds with older retirement products will need to establish significant programs of work and associated member communications to support this reform.

Other superannuation changes scheduled for 1 July 2021

Many superannuation rates and thresholds are reviewed and may change each 1 July. These changes take place independent of the Budget changes.

Here are some of the key rates that change on 1 July 2021:

SG employer contributions increase from 9.5% to 10% of earnings.

Maximum super contribution base increases from $57,090 to $58,920 per quarter.

Concessional contributions cap increases from $25,000 to $27,500.

Non-concessional contributions cap increases from $100,000 to $110,000.

Superannuation co-contribution lower-income threshold increases from $39,837 to $41,112; higher-income threshold increases from $54,837 to $56,112.

Transfer Balance Cap increases from $1.6 to $1.7 million.

IQ is well placed to support super funds through these changes and we look forward to working with clients to navigate the complexity and ensure all stay on track for success.

By Kath Forrest (Head of Strategic Growth and Capability)

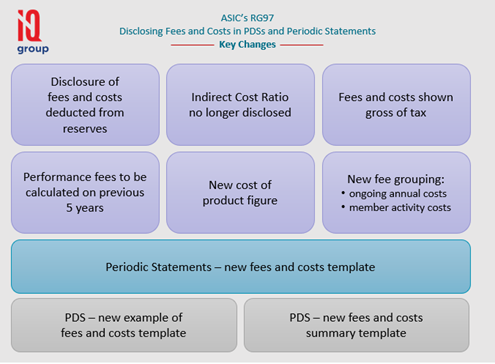

ASIC’s fee and cost disclosure regime has been a journey of twists and turns for the superannuation sector and the road ahead doesn’t look any straighter. Whilst disclosing fees and costs in Product Disclosure Statements (PDSs) and periodic statements sounds simple enough, it is costing super funds millions of dollars to get it right. Let’s take a brief look at why RG97 is ‘tangled with good intentions’.

Why is RG97 needed?

High administration fees erode member balances and has the potential to put a big hole in the retirement savings for many. Consumers require consistent and transparent communication when it comes to fees and costs in order to understand the difference between ‘high’ and ‘low’ fees and consider the impact that fees and costs has on their retirement income.

What does RG97 contain?

RG97 provides guidance for issuers of superannuation products and managed investment products on how fees and costs should be disclosed in PDSs, short PDSs and periodic statements. The purpose of fees and costs disclosure is to ensure that consumers have accurate information to help them make confident and informed ‘value-for-money’ decisions, compare products and understand the fees and costs charged to them.

When does RG97 apply?

PDSs given from 30 September 2022 must meet RG97 requirements, although issuers have been able to apply them since September 2020. Periodic and exit statements with reporting periods commencing on 1 July 2021 must comply with the new requirements, meaning that the new requirements for exit statements will be triggered for exits on or after 1 July 2021.

What are the key issues?

Issue 1 – a prescriptive framework

The legislative framework for fees and costs disclosure is prescriptive and can present many complex compliance challenges for funds. One of the aims for RG97 is for the fees and costs disclosure regime to be practicable to apply for industry while ensuring consumer objectives are met. Applying a prescriptive framework for super and managed investment products that are on very different platforms is difficult, as pricing can be complex and multi-layered.

Issue 2 – potential to misinform

Some super funds are increasingly lowering their fees and costs in order to stay competitive in the market and some products can be made to look cheaper, and more competitive, than others when in fact they have the same costs. Whilst ASIC has the power to stop disclosure that does not meet legal requirements, consumers can be left misinformed in the process.

Issue 3 – platform products vs direct investments

Platform operators that provide products such as Master Trusts or lnvestor Directed Portfolio Services (IDPS) could, in theory, reduce overall fees as they are pooled. These fees may apply to administration, moving money in and out, investment management and service. Platform products have a more complex structure and therefore disclosure is also going to be more complex than for non-platform products like “self-directed” investment products.

As the super industry continues to grapple with the fees and costs disclosure regime and ‘untangle’ these key issues, RG97 is ultimately an attempt to further enforce consistent and transparent disclosure of fees and limit the ability for a fund to appear more competitive to consumers than it actually is. While presenting compliance challenges for super funds, any misleading claims about low fees will be treated very seriously by ASIC and the Regulator will continue to intervene against inadequate disclosure.

Overall, disclosure of any means within financial services is tricky and complicated. Regulatory guidelines, such as RG97, will always include hotly contested issues, however it is up to the super industry to work together with the Regulator to navigate the complexities. Accurate disclosure is critical to prevent misinformation and prevent superannuation members remaining confused, disengaged and potentially disadvantaged when it comes to maximising their retirement incomes.

IQ consultants are the leading experts in regards to legislative changes. Across all of our three key services: Advisory; Delivery and Managed Services, we excel in our proactive understanding of how each fund is unique and we build trusting relationships with funds in order to navigate complexities, like those within RG97, and create individual pathways to success.

Following on from my previous post “Retirement Income Review: Robust or Rabbit Hole”, the RIR Report was released by Government on 20 November last year. The Government has not officially commented on the RIR yet but, as we are getting closer to the June Federal Budget and the 1 July legislated date for an increase in Super Guarantee (SG) to 10%, we are seeing the market commentary ratcheting up a notch or two. The ‘should it increase?’ or ‘should it not increase?’ debate will continue until the Government provides confirmation one way or the other.

The focus for this post, however, is not on SG but rather on the RIR’s findings regarding home ownership, specifically how it impacts on retiree’s ability to maintain their standard of living in retirement.

Before I jump-in, I’d like to revisit the purpose of superannuation (a key part of the Australian Retirement System). It was introduced to help Australians save for retirement during their working lives and reduce or minimise reliance on the Aged Pension. As the population continues to age and the number of working people supporting each retiree (over 65) decreases (having gone from 6 to 3.7 and projected to be at 3 soon), we need to continue saving and using retirement savings for their intended purpose if the system is to stay successful.

An important finding from the RIR was that the system favours home ownership (specifically mortgage free by age 65) as a way of substantially improving the likelihood of a person maintaining their lifestyle during retirement. However, house prices have been growing much faster than income over the past 30 years and it is taking first home buyers longer to save that initial deposit. This can lead to more people carrying a mortgage into retirement. Later entry into the housing market could lead to lower levels of home equity than previous generations, also consider the fact that we are living longer, and the result is a significant impact on retirement drawdown strategies. With interest rates at historical lows and house prices in the major cities being fueled by what some suggest is a healthy case of F.O.M.O., the dream of owning a home and more practically using this as an asset in retirement is becoming ever more unachievable.

Against this backdrop, the call from some ministers to use superannuation as a deposit for first home buyers seems irresponsible. There is a need for affordable housing and there is equally a need NOT to put further fuel on an already flaming hot property market. A holistic and carefully considered approach is required and not one dimensional, populist politics that may do more harm than good.

At the start of the pandemic, the Government dipped into the superannuation cookie jar by offering the Early Release Scheme (ERS) to support Australians caught between impossible choices. Choices between struggling today or potentially struggling in retirement. The Government had to act quickly with uncertain information, and they did. However, it is time to firmly close the cookie jar and go back to continuing with super’s intended purpose while working towards an affordable housing solution that will benefit all Australians and support, rather than detract, from the parts of the retirement system that are already delivering benefits.

The RIR found that Australia’s retirement income system is effective, sound and its costs are broadly sustainable. This achievement is often glossed over on the way to making a point about something in particular but let’s take a moment to celebrate this success.

Our superannuation system has been rated as the 4th best in the world and no structural issues were identified that require wholesale changes for the system to continue functioning into the future. It is perfectly reasonable to continuously monitor, review and tweak the system. However, we need to be careful to not use savings in the superannuation system as the cure for all ills in the economy… going down that rabbit hole may have a price to pay down the line.

Recent Comments