We must trust super funds to deliver our best outcome possible in retirement and we should expect the same level of responsibility and commitment when it comes to dispute resolution.

In 2010 I studied SIS Legislation. At the time, I understood the R in RSE (Registrable Superannuation Entity) to mean ‘Responsible’. It was an easy mistake to make.

Here we are a decade later and the Government’s regulatory agenda, post Royal Commission, is systematically improving the financial services industry in Australia, restoring integrity to its pillars and ultimately ensuring that ‘responsibility’ is NO mistake when it comes to RSEs.

Dispute Resolution, which sits at the very core of any responsible organisation, is of course a key focus of the regulatory agenda. As a result of the COVID-19 pandemic, we’ve seen depression-level financial hardship and consumer vulnerability, so ASIC considers it essential that Internal Dispute Resolution (IDR) performance is significantly improved. Successful IDR processes go a long way to reducing customers’ emotional grievances (which is a leading cause of escalations) and help to improve products and services through effective use of complaints data. This ultimately reduces the overall number of complaints and improves responsibility over time.

The report also highlighted that data on Internal Dispute Resolution (IDR) outcomes was limited and inconsistent across organisations and the effectiveness of IDR processes could not be determined. It recommended the establishment of industry standard reporting. ASIC’s RG 165 was revised and in July this year the regulator published RG 271 Internal Dispute Resolution, outlining updated IDR standards and requirements which take effect on 5 October 2021.

Here’s a look at what’s changing:

1.Updating the definition of ‘Complaint’2

A complaint will be considered as “[An expression] of dissatisfaction made to or about an organization, related to its products, services, staff or the handling of a complaint, where a response or resolution is explicitly or implicitly expected or legally required.”

By broadening this definition, social media will now be a legitimate complaint channel. Funds are also being directed to take an active approach to identify complaints. Initially, the interpretation meant funds would need a dedicated resource to trawl through digital platforms for any kind of wording about them. Instead, complaints are to be identified on accounts owned by the fund and the complainant must be identifiable and contactable.

2. Reduced Timeframes3

In research conducted by Nature and published in ASIC’s Report 603 The Consumer Journey through the Complaint Resolution process of Financial Service Providers, 86% of superannuation complaints were concluded within the previous timeframe of 90 days. Below is a table of the new timeframes:

Type of complaint

Current maximum

New maximum

Superannuation and traditional trustee services

90 days

45 days

Superannuation death benefit distributions

90 days

90 days

Other financial services complaints

45 days

30 days

Different timeframes apply to:

complaints about a traditional trustee (see RG 271.76–RG 271.78);

complaints about superannuation trustees (see RG 271.79);

complaints about superannuation death benefit distributions (see RG 271.80–RG 271.85); and

certain types of credit complaints (see RG 271.86–RG 271.101).

3. Reasons for Decisions are Adequately Explained

Complaint responses are often too reliant on system-generated responses and automation capability which does not provide rationale for decisions specific to individual complaints. Data gathered from consumer research said 43% of complainants believed the rationale for the decision is important and 25%, extremely important4.

When a financial firm rejects or partially rejects a complaint, the IDR response will need to clearly set out the reasons for the decision by:

identifying and addressing the issues raised in the complaint;

setting out the financial firm’s findings on material questions of fact and referring to the information that supports those findings; and

providing enough detail for the complainant to understand the basis of the decision and to be fully informed when deciding whether to escalate the matter to AFCA or another forum.

4. IDR Standards (Enforceable)

The appendix of RG 165 contained guiding principles against each of the 4 Requirements Sections of the Guide. In RG 271 there are 34 Enforceable Standards across 8 Requirements Sections:

Commitment and Culture

Enabling Complaints

Resourcing

Responsiveness

Objectivity and Fairness

Policy and Procedures

Data Collection, Analysis and Internal Reporting

Continuous Improvement

5. Identifying and Escalating Systemic Issues

While Nature were compiling the research for ASIC’s Report 603, ASIC were conducting on-site visits to have a look at what funds were doing, when they identified issues impacting multiple members. General observations showed that systemic issues were not proactively identified or addressed. Complainants would often pursue External Dispute Resolution processes before Funds began to rectify an issue.

In RG 271, systemic issues complaints ending up at AFCA will be reported to the regulator within 15 business days.

These changes to dispute resolution, along with all the other regulatory changes to be implemented will, of course, take a lot of grit and determination from all who are involved. However, IQ comprehensively understands what these changes mean and is committed to helping clients sail through the rising tide of regulatory transformation washing over the industry.

Whilst it may have been a mistake, on my part, to think that the R in RSE meant ‘Responsible’, I’ll consider it a Freudian slip. “Responsibility” is exactly what the Government is enforcing and the financial services industry has a bright future, as do we … its customers.

By David Shortt (Operations Consultant)

1 Page 187 https://treasury.gov.au/sites/default/files/2019-03/R2016-002_EDR-Review-Final-report.pdf April 2017 2 Australian Securities and Investments Commission, https://download.asic.gov.au/media/5720607/rg271-published-30-july-2020.pdf July 2020, Page 13. 3 ASFA Virtual Workshops: The updated Internal Dispute Resolution (IDR) procedures Under RG 271 Tuesday 20 October, 10.00am–11.00am 4 Nature, https://download.asic.gov.au/media/4959291/rep603-published-10-december-2018.pdf December 2018, Page 63

To date, the implementation of Protecting Your Super (PYS) and Putting Members Interests First (PMIF) legislation has been a long and winding road and this will continue, with even more twists and bends, as the next round of changes come through.

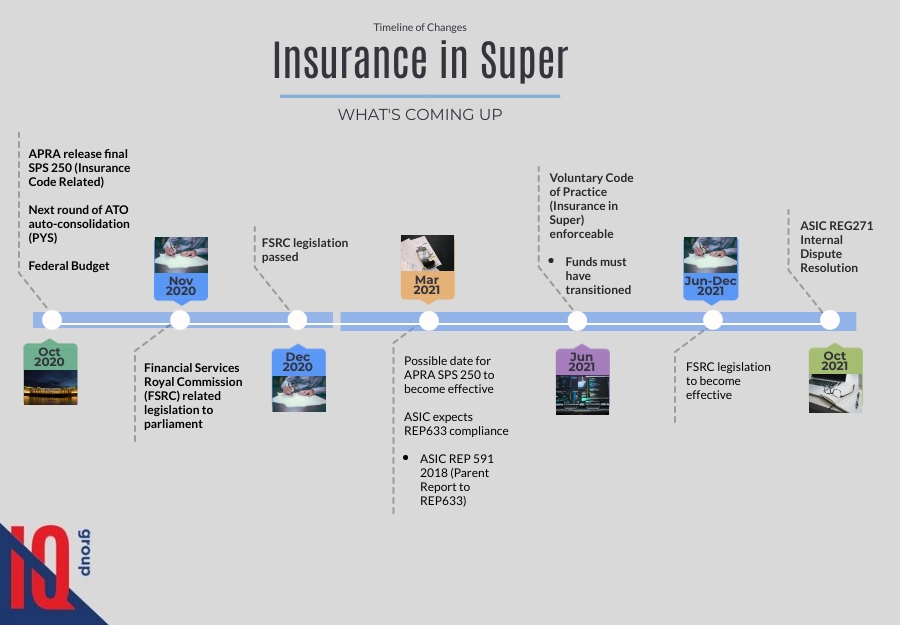

The last two years have seen a myriad of changes to superannuation and its affiliated insurance but in the words of Billy Ocean ‘when the going gets tough, the tough get going’. It’s been great to see the industry take on these changes, to prioritise and protect members’ interests, with focus and determination. The year ahead will be one of the toughest yet, so let’s have a look at what’s coming up in regards to insurance in super.

Oct 2020APRA SPS 515 Strategic Planning and Member Outcomes: annual performance assessment to determine whether the financial interests of the members are being promoted; Federal Budget implications; next round of ATO auto-consolidation (PYS).

Dec 2020 Implementation of various FSRC related legislation: enforceability of industry codes (eg. Insurance in Super Code of Practice), Insurance Claims handling to become a financial service; Universal Terms for Insurance in MySuper.

Mar 2021APRA SPS 250 Insurance in Superannuation: requirements with respect to making insured benefits available to beneficiaries; Compliance with ASIC REP633: requirements set to provide improved consumer protections which many funds will be able to meet as they renegotiate their insurance policies.

Apr 2021Design and Distribution Obligations and Product Intervention Powers Regime: Issuers and distributors required to have an adequate product governance framework to ensure products are targeted at the right people (this regime will affect almost all areas of the financial services industry).

Jun 2021Insurance in Super Voluntary Code of Practice becomes binding and enforceable and funds must have transitioned and be compliant before this date.

Oct 2021ASIC REG271 Internal Dispute Resolution: financial entities must meet ASIC’s standards and requirements for Internal Dispute Resolution systems and have an AFCA membership.

Dec 2020-21Financial Accountability Regime: extension of accountability requirements to other APRA-regulated entities and directors/senior executives in accordance with the government’s response to the FSRC recommendations.

OngoingAFCA implementation and compliance

UnknownPotential creation of a co-regulatory model for industry codes: Under a co-regulatory model, industry participants would be required to subscribe to an ASIC approved code and, in the event of non-compliance with the code, an individual customer would be entitled to seek appropriate redress through the participant’s internal and external dispute resolution arrangements.

As well as ensuring compliance and implementation of all regulatory and legislative changes, super funds will still be dealing with the continuing ramifications of COVID-19. IQ remains focussed on helping our clients navigate these changes and cut through the complexity of the year to come, supporting them to achieve the best outcomes for their members.

The insurance world keeps turning and regulations and standards are constantly evolving, but members still need their insurance and funds must continue to put members interests first, in everything they do.

By Kiara Leslie (Graduate Consultant) and

Sharon Campanaro (Principal Consultant and Head of Change and Learning Services)

As we wait for the Retirement Income Review report to be released, we thought we’d ask one of our very own, George Georgiou, how he feels personally about getting closer to retirement and find out just how good the superannuation system, in particular, has worked for him.

George, please tell us a bit about yourself. What are your likes, dislikes?

I’m in my 60s and married with 3 adult daughters. I enjoy spending time with family and watching my beloved Tigers. What I dislike is spending time commuting and seeing the Tigers lose!

What’s your dream retirement?

It’s important to me to retire with good health, and not ‘work myself to death’, so whilst I am feeling ok and making a contribution I will keep working. The move to working from home has helped me a lot, not having to travel for 3 hours a day. This has been a factor in my thinking about transitioning to retirement in a stage approach. Once I retire, I think there will be some travel, local and overseas, but spending time with family and friends will be important to me.

Are you likely to live out your dream retirement?

I hope so – the cost of living is going up all the time, so I keep trying to put money into areas that will save me money once I am retired – home renovations are top of the list.

What will be most important to you in retirement?

The most important things for me will be good health – to be able to do the things I want to do; no pandemics to interfere with my holiday plans; and an income – that supports the lifestyle I want to have.

Have you planned for your retirement and if so, how?

I am putting some extra dollars into super each pay day to help boost the final balance. I am making sure that I don’t take have any debts when I get to retirement age. Also, we are looking to manage our lifestyle to spend less each week.

What has the current pandemic highlighted for you and does this affect your plans?

The pandemic has made me realise how much time was lost travelling into the office every day. Working from home will now be a constant part of my remaining work life. I feel that I now have the ability to work longer than might have been the case if I had to continue to commute every day to work.

How do you feel about getting closer to retirement?

I am reasonably confident as my super balance has not been greatly impacted by the pandemic – a zero return for the last year is about all I could have expected. Using the calculator on my fund’s website says I need to keep contributing a little extra regularly to my super to ensure my retirement income meets my lifestyle.

What has your experience of the superannuation system been like?

Super is a very major part of my retirement planning. I only moved from a retail fund to an industry fund 5 years ago and, looking back, I wish I had moved earlier. The clarity of the reporting from the industry fund has made it much easier for me to understand where my money is invested and the returns it is generating – this was not there 5 to 10 years ago.

I feel that having the flexibility to choose where my money is invested is a positive feature, especially if you believe that you would prefer your savings to be invested in the industries you support rather than those selected by your fund’s investment committee.

As you get closer to retirement, what message do you have for people younger than you?

I encourage everyone to look at the lifestyle of your seniors or parents, and ask if they have the lifestyle that you would like to have when you reach their age.

Consider how they have achieved that lifestyle, positive or negative, and ask yourself what lessons you can learn from their position. Then, set the plans in place to achieve your preferred retirement lifestyle.

As part of the Federal Budget, the Government’s Your Future, Your Super reforms have been announced. Provided the measures are passed by Parliament, by 1 July next year, the following changes will take effect.

Stapling Employees to a Super Fund for Life

Employees will keep their super fund when they change jobs, and thus stop the creation of unintended multiple super accounts and the erosion of super balances.

Employers will pay super to an employee’s existing super fund unless the employee selects an alternative fund. Employers will obtain information about an employee’s existing super fund from the ATO by logging onto ATO online services.

If an employee does not have an existing super account and does not make a decision regarding a fund, the employer will pay the employee’s superannuation into their nominated default fund.

YourSuper Comparison Tool

A new, interactive, online comparison tool will help members decide which super product best meets their needs. The YourSuper tool will:

Provide a table of simple super products (MySuper) ranked by fees and investment returns.

Link to super fund websites where members can choose a MySuper product.

Show a member’s current super accounts and prompt them to consider consolidating if they have more than one.

Annual Super Fund Performance Test

MySuper products will be subject to an annual performance test.

If a fund is determined to be underperforming, it will need to tell its members of its underperformance by 1 October 2021.

When funds communicate their underperformance to members, they will also be required to provide information about the YourSuper comparison tool.

Underperforming funds will be listed as underperforming on the YourSuper comparison tool until their performance improves.

Funds that fail two consecutive annual underperformance tests will not be permitted to accept new members. These funds will not be able to re-open to new members unless their performance improves.

By 1 July 2022, annual performance tests will be extended to other superannuation products.

New Best Financial Interests Test for Trustees

Trustees will be required to comply with a new duty to act in the best financial interests of members.

Trustees must demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests.

Trustees will provide members with key information regarding how they manage and spend their money in advance of Annual Members’ Meetings.

The Federal Budget did not announce any change to early release arrangements, freezing the SG, or launching an insurance review.

IQ have been full steam ahead in working through the many changes that are happening within the superannuation industry and our clients are well and truly supported by our consultants as we work through the challenges at play whilst in the midst of a global pandemic. Australians deserve a top-class retirement income system and, whilst some changes on the horizon require careful consideration and negotiation in order to ensure better outcomes for all, we are heading in the right direction.

Recent Comments